Metavaults Deep Dive: Backtest & Benefits

"Metavaults allow users to farm LPs while hedging both tails of probability in the presence of volatility, improving the payout profile of their LP position in a completely principal-protected manner."

Overview

When a user enters a traditional LP position, they typically forgo the upside and expose themselves to downside risk. Moreover, the user’s downside exposure increases with more downside and their upside exposure decreases with the more upside there is. For maximizing return, this is not ideal!

Metavaults allow users to farm LPs while hedging both tails of probability in the presence of volatility, improving the payout profile of their LP position in a completely principal-protected manner. Principal-protected is in reference to principal denominated in the deposited LP tokens. Additionally, Metavaults significantly reduce the effect of impermanent loss.

For a given LP, Metavaults require the user to select a ‘Bull’ or ‘Bear’ bias, and deposit the corresponding LP tokens. The LP tokens are staked in the underlying farm and part of the yield is used to purchase either calls (Bull) or puts (Bear) on the price of $ETH.

Backtests show that if a user had stayed in any Metavault for the past year, their yield would have been similar to or slightly higher than the underlying LP farm. This is by design — it is Jones' intention that users will select Bull or Bear vaults depending on their market outlook, instead of staying in one vault the entire time. With the right bias, their yield is enhanced. Therefore, at worst, users earn a similar yield to the underlying LP farm, and at best, greatly enhance their LP’s overall yield profile.

Benefits

LP Principal-Protected Alpha

In annualized terms, the user enhances their LP position with a hedge (protecting from the tail risks) with no upfront costs. The performance of the Metavaults will vary for each user depending on their selected bias. Some epochs may produce additional gains, while others may result in a smaller but still positive APR.

- Best case scenario: Tails hedged, extra yield during volatility, amplified LP payoff.

- Worst case scenario: Tails hedged, similar yield to the original yield from the underlying LP farm.

The principal is denominated in the LP tokens deposited, not in the USD value of the position. Funds from the principal deposit are not used for options exposure, hence, in the LP-token terms, the Metavaults are principal-protected.

Built-in Auto Compounding

The Metavaults autocompound LPs and give users significant quality-of-life upgrades, while automatically boosting yield. Most autocompounders charge 20%, but the Metavaults charge 0% for autocompounding—It’s just an added bonus for a better user experience.

Effective Automated Hedging

Metavaults excel at hedging tails of price volatility. During the FTX fiasco, The Bear Metavaults would have produced ca. 2.40% ROI during the corresponding weekly epoch (which translates to 250%+ APR when extrapolated from that week)

To take full advantage of the fast execution environment on Arbitrum, the Metavaults have keepers that automatically snipe options at desired strikes the moment they’re available. This provides Metavault users with a unique advantage wherein users buy the most popular strikes before they sell out.

Simulated Historical Performance

Methodology

Using historical price data (2021 December to 2022 December) for ETH, DPX, and rDPX; a vanilla LP position was simulated for both DPX-WETH and rDPX-WETH. Then, another instance of the LP was simulated for both Bull and Bear Metavaults, with the functionality of the Metavaults applied to the behavior of the LPs.

Available option strikes were assumed to be at the money, which have a 3% premium cost for 3.5 day options. The base yield from emissions for all LPs was assumed to be 28%. The performance of the vanilla LP vs. Bull Metavault vs. Bear Metavault was compared for both DPX-WETH and rDPX-WETH.

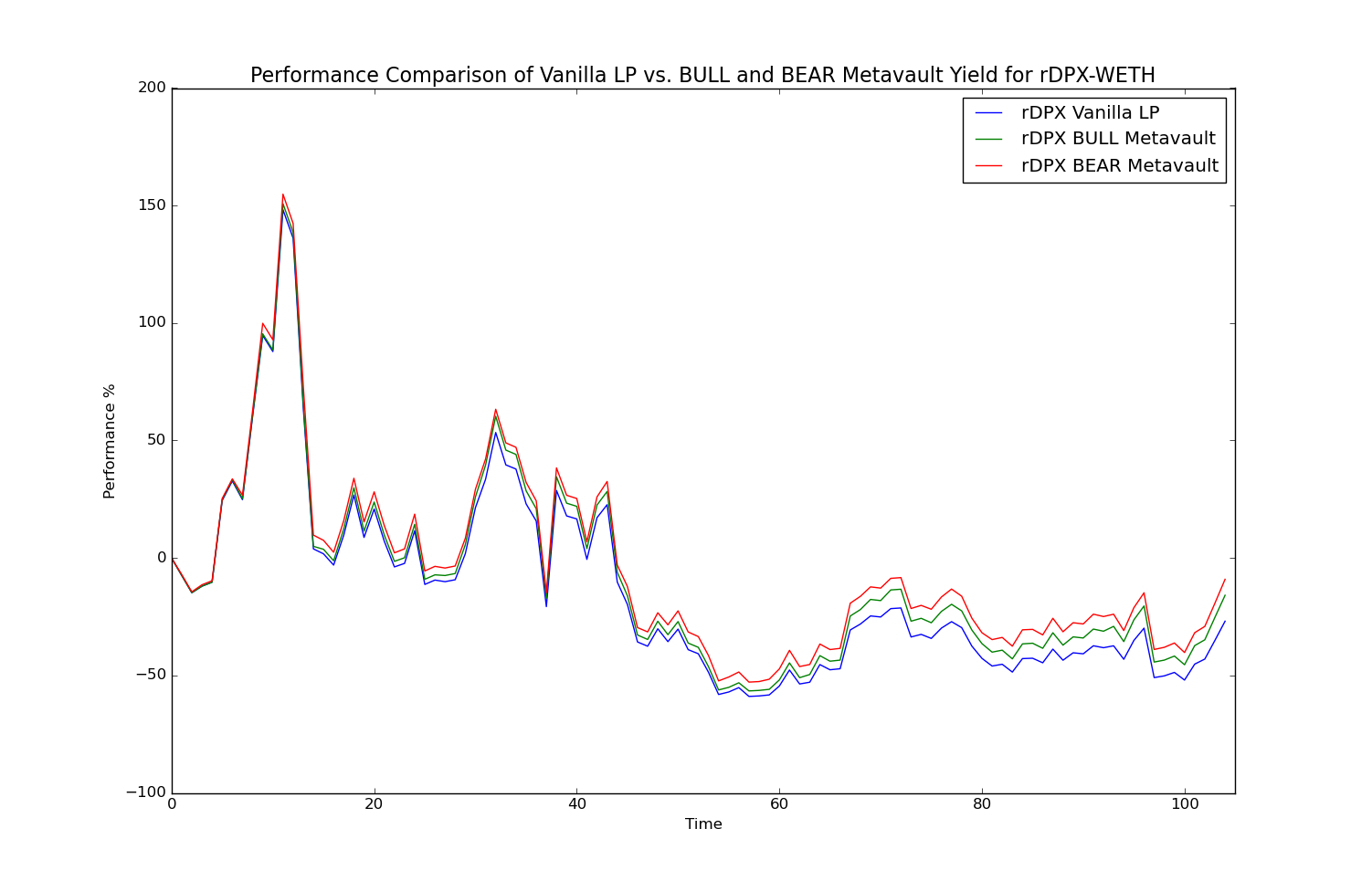

rDPX-WETH LP

DPX-WETH LP

Key Takeaways

Both the Bull and Bear Metavaults for the DPX and rDPX LPs outperformed the vanilla LP on an absolute and relative basis.

On an absolute basis, Metavaults would have mitigated a large portion of the downside experienced by the vanilla LP strategy during recent poor macro conditions. The rDPX-WETH Bear Metavault’s drawdown was only -9.076%, compared to the vanilla LP’s drawdown of -26.907%.

Likewise, the DPX-WETH Bear Metavault’s drawdown was only -58.513%, compared to the vanilla LP’s drawdown of -67.024%.

Significant alpha is further showcased by the Bull and Bear Metavaults’ relative performance to the base performance of the vanilla LP.

Notably, the rDPX Bear Metavault performed exceptionally well relative to the vanilla rDPX LP: 17.831% simulated historical returns were recorded once the negative performance of the base vanilla LP (and thus the macro backdrop) was subtracted.

Meanwhile, the DPX Bear Metavault also exhibited 8.511% simulated historical returns on a relative basis.

We hope this article helps to articulate and exemplify some of the benefits of our Metavaults. Jones is always driven by bringing best-in-class yield strategy products to our Jonesies and Metavaults is no exception!

None of this article is to be interpreted as financial advice. DYOR.

Join the Jones DAO community now to stay up to date on our upcoming releases and partnership announcements. We’ll be hosting AMAs, previews, and sharing plenty of alpha: